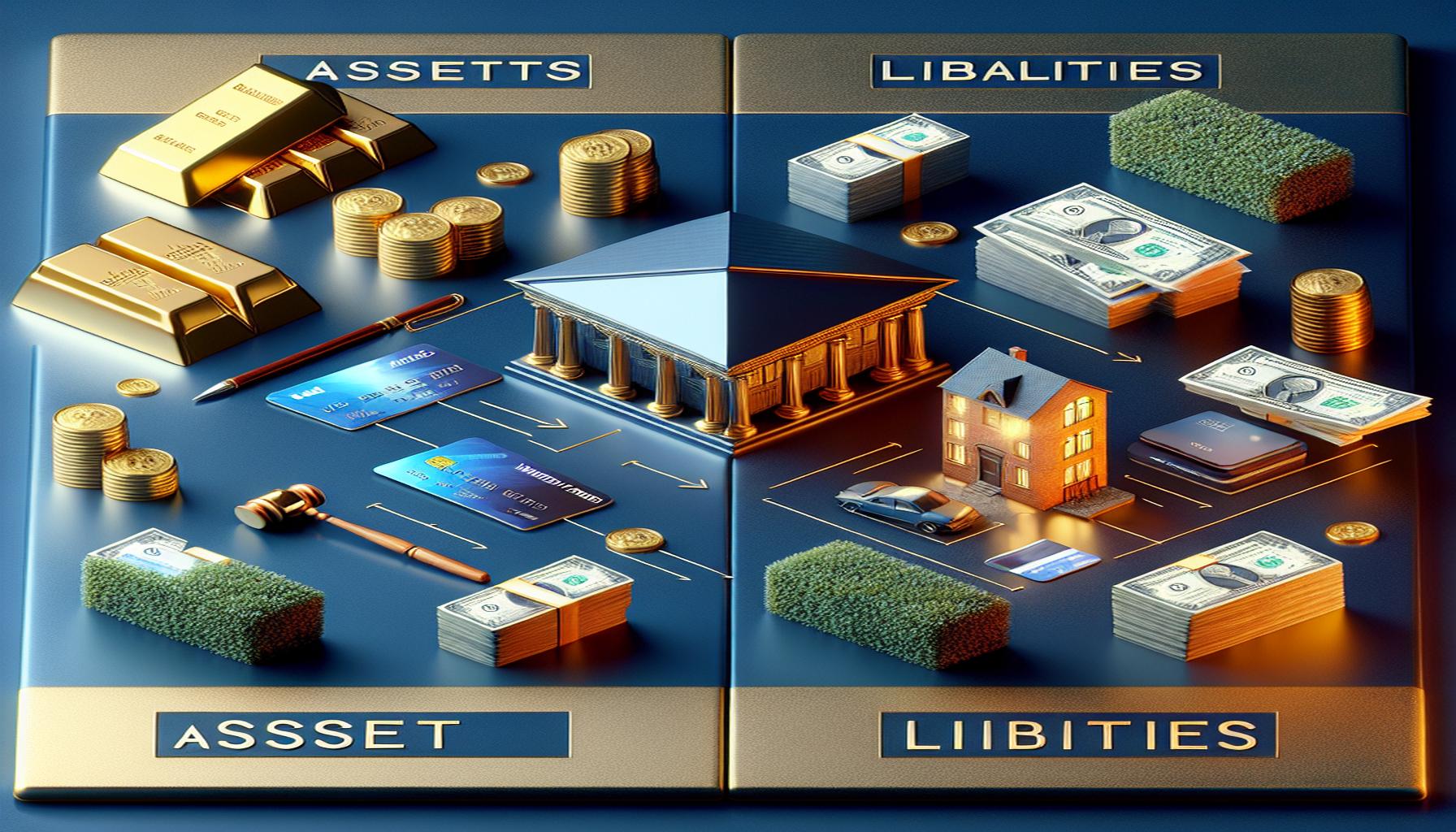

Difference between assets and liabilities in financial education

Key Components of Your Financial Health

In the realm of personal finance, having a solid grasp of assets and liabilities is vital for effective financial management. These two fundamental concepts form the basis of your financial status and can significantly influence your decision-making process. Understanding these components not only helps you assess your current financial health but also enables you to strategize for a more stable and prosperous future.

Assets are essentially the resources you possess that can generate value or income over time. They can take various forms, and having a diverse array of assets can enhance your financial security. Common examples of assets include:

- Cash in your bank account: This is the most liquid form of asset, readily available for expenses or investments.

- Investment properties: Properties purchased to generate rental income can be a significant source of cash flow and appreciation.

- Stocks and shares: Investments in companies via shares can yield dividends and increase in value, contributing to long-term wealth.

- Vehicles and other valuables: While cars often depreciate, classic or collectible cars can appreciate in value, making them worthwhile assets.

Conversely, liabilities refer to the financial obligations or debts you are required to repay. Understanding your liabilities is crucial, as they directly impact your net worth and cash flow. Typical liabilities include:

- Mortgages: Loans taken out to purchase property. This long-term liability often represents the largest portion of personal debt for many Australians.

- Personal loans: These loans can be used for various purposes, such as financing a car or home renovations, but they require careful management to avoid falling into debt.

- Credit card debt: Often associated with high-interest rates, this liability can quickly accumulate if not paid off promptly. It’s essential to manage credit card usage wisely.

- Outstanding bills: Regular bills, such as utilities and subscriptions, contribute to your financial obligations and must be factored into your budgeting.

By comprehensively understanding the distinctions between assets and liabilities, you equip yourself to build a robust financial future. This insight is pivotal in developing a balanced budget, encouraging savings, and ultimately leading you toward financial independence. Always remember that the goal of sound financial management is to maximize your assets while minimizing liabilities, creating a pathway toward achieving your financial aspirations. With a careful approach and ongoing education, you can navigate your personal finances confidently and effectively.

Understanding the Distinction between Assets and Liabilities

To effectively navigate the world of personal finance, grasping the fundamental differences between assets and liabilities is essential. While both elements are necessary to paint a complete picture of your financial status, they serve opposite purposes and can have a significant impact on your overall wealth. Fostering a clear understanding of these concepts can empower you to make informed decisions that align with your financial goals.

Assets: The Building Blocks of Wealth

Assets are the economic resources you own or control that have the potential to generate future economic benefits. They can be categorized into several types, reflecting their source of value or the way they contribute to your financial stability. Some key types of assets include:

- Liquid Assets: These are assets that can be easily converted to cash without losing value. Examples include money in your savings account and short-term investments.

- Fixed Assets: These are tangible items that you own, such as property, vehicles, or equipment, which are not intended for resale but provide long-term benefits.

- Investments: Investments in stocks, bonds, or mutual funds can create wealth over time through appreciation and earnings.

- Intangible Assets: These include non-physical assets such as patents, trademarks, and intellectual property that can provide value.

The goal of accumulating assets is to enhance your net worth, allowing you the financial freedom to invest in opportunities, save for retirement, or cover unexpected expenses. A diverse asset portfolio can significantly reduce financial risk while fostering long-term growth.

Liabilities: The Burden of Debt

On the flip side, liabilities encompass the financial obligations that require you to pay out money in the future. Unlike assets, which contribute positively to your financial health, liabilities can strain your resources if not managed carefully. Here are some types of common liabilities:

- Long-term Liabilities: These typically represent major financial commitments, such as mortgages that span several years or decades.

- Short-term Liabilities: This category includes debts that need to be paid off within a year, such as personal loans or some credit card balances.

- Recurring Financial Obligations: Regular expenses, such as utility bills or subscriptions, also fall under liabilities and should be accounted for in your budgeting.

Understanding and managing your liabilities is crucial, as they compete for your cash flow and can influence your creditworthiness. By monitoring your liabilities closely, you can develop strategies to minimize debt and avoid financial pitfalls.

In summary, assets and liabilities are two sides of the financial equation. While assets work to propel you toward your financial aspirations, liabilities can hinder your progress if not monitored judiciously. Striking the right balance between the two is fundamental to building a solid financial foundation.

The Impact of Assets and Liabilities on Financial Health

Recognizing the differences between assets and liabilities is not just an academic exercise; it has practical implications that can dramatically influence your financial well-being. A strong grasp of these concepts can help you manage your money more effectively, strategize for the future, and avoid common pitfalls.

The Importance of Asset Accumulation

Building a robust portfolio of assets is crucial for achieving financial independence. You might consider real estate investments as a prime example; purchasing an investment property in Australia can provide both rental income and capital appreciation over time. Additionally, investing in superannuation funds can be a smart way to build retirement savings while taking advantage of tax benefits. Investments in stocks and bonds can actually produce wealth that outpaces inflation, increasing your purchasing power in the long run.

However, it’s essential to not only focus on acquiring assets but also to evaluate their potential for growth and income generation. For instance, some assets, like high-end vehicles, may depreciate quickly and provide little to no return on investment compared to alternative assets such as commercial properties or indexed funds that track the performance of the stock market.

The Consequences of Excessive Liabilities

While managing your assets is imperative, keeping an eye on your liabilities is equally important. An excess of liabilities can lead to financial instability and stress. Consider a scenario where you have taken on a large mortgage with correspondingly high interest payments; this can consume a significant portion of your cash flow, leaving less room for savings or investments. In Australia, where property values can fluctuate, being over-leveraged can expose you to market risks that might lead to negative equity, where you owe more on your mortgage than the property is worth.

Another common area of concern is credit card debt. With the average credit card interest rate hovering around 15-20%, carrying a balance can quickly become a financial burden. It’s essential to prioritize paying off high-interest debts to free up resources for more productive uses, such as investing in growth assets. Educating yourself about effective debt repayment strategies, like the snowball or avalanche method, can empower you to reduce your liabilities systematically.

Balancing Assets and Liabilities for Financial Stability

Achieving a healthy balance between assets and liabilities is key to enhancing your financial health. Tools like net worth calculators can be immensely helpful in determining where you stand. By subtracting your total liabilities from your total assets, you can gain clarity on your net worth and adjust your strategy accordingly. A positive net worth indicates that your assets exceed your liabilities, a vital indicator of financial stability.

Moreover, it’s beneficial to establish a financial plan that factors in both your income and expenses, aiming to build assets while managing liabilities effectively. For instance, setting up automatic transfers to a savings account or investment account can create a habit of saving that enhances your asset base over time. Ultimately, by remaining conscious of both sides of your financial equation, you can secure a more stable financial future.

Conclusion

Understanding the difference between assets and liabilities is fundamental to achieving financial literacy and better money management. By recognizing what constitutes an asset—anything that puts money in your pocket—and what qualifies as a liability—anything that takes money out of your pocket—you can make informed choices that directly affect your financial health.

Prioritizing asset accumulation is a key strategy for building wealth and securing financial freedom. For Australians, investing in tangible assets like real estate or managed funds can enhance your net worth while also providing valuable avenues for generating income. On the other hand, being vigilant about your liabilities helps protect you from financial stress. Avoid accumulating excess debt, particularly high-interest obligations like credit card balances which can quickly spiral out of control.

Ultimately, striking a balance between assets and liabilities will empower you to craft a sustainable financial future. Regularly assessing your financial situation through tools like net worth calculations will provide insight into your progress and areas for improvement. Establishing a robust financial plan that incorporates strategic savings and investment habits can help you work towards a secure and prosperous financial life. By adopting these practices, you will not only enhance your understanding of financial concepts but also position yourself for long-term success in managing your finances effectively.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the Take Care Garden platform. Her goal is to empower readers with practical advice and strategies for financial success.